Our daily way of life is going to change completely. It’s basically going to come to halt. People will lose jobs. People will lose their businesses. We won’t be able to gather for holidays. You’ll have to wear a mask everywhere you go.

One year ago today, had you said the above things to me, I wouldn’t have believed you. Yet here we are.

This past year has felt much longer than others for many reasons. Unfortunately, it may be the remainder of this year before we begin to see a return to normalcy. But what does that mean? “New normal” and “work-life integration” are buzz words our society has been using for the past several months as we realize our way of life has changed permanently.

COVID has made us rethink how we operate as a society, not just personally but professionally as well. In March, I thought for sure we would be back to business as usual by July at the latest and as the new year dawned, we are still not “business as usual”.

I don’t think we will ever go back completely to the way businesses operated prior to COVID. Too many conveniences have been demonstrated to simply turn back. For instance, virtual meetings and remote work have provided many employees and business owners with a new perspective of work-life integration and expense control that will remain desirable moving forward.

At the beginning of the pandemic, those of us employed in the insurance industry breathed a sigh of relief as governors around the country began to declare insurance essential business. Some agencies were able to transition to a virtual office environment easily while others continued to bring staff in but with restrictions. The fact that we could keep our doors open, care for our customers, and keep our staff employed was a huge win for our industry.

VIRTUAL IS HERE TO STAY

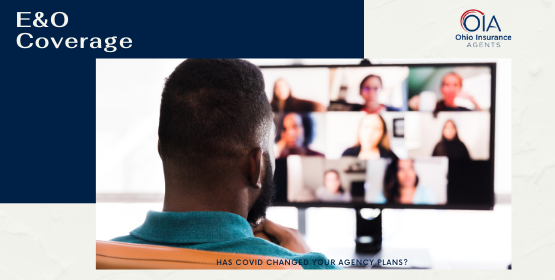

We are living in a virtual world more now than ever. Investing in digital and website automation will be necessary moving forward as consumers are embracing a more virtual world. This is not to say the human interaction isn’t necessary. I believe it will always be necessary on some level, but potential clients need to be able to google search and find your agency. Clients will want the ability to interact with you on different mediums and at times that are convenient for their lifestyles. Change is here and you may be looking for a way to handle that change.

All of the turmoil from COVID may have you thinking about the future of your agency in a different way. Some owners may be struggling to change to meet the demand of a workforce who is seeking the work-life balance of remote work. The investment in technology to offer that as an option may not be appealing if you are nearing retirement. Revenue reductions due to lost business, premium refunds, and exposure decreases may have you concerned about your financial future.

OIA IS HERE TO HELP

With all these changes to the marketplace, we want you to know, you are not alone. OIA has resources available that can help you no matter what you are contemplating. If you need help to modernize your agency, we have on-staff consultants that can help you determine technology needs, business planning, streamlining operations, and much more.

If you are considering retiring a little earlier than planned or merging with another firm that may have the resources necessary to compete moving forward, you have resources available to you at OIA.

OIA E&O POLICYHOLDERS

If you are contemplating merging or retiring, remember, OIA is the agent’s agent. All too often we, your agent, are not notified of an agency’s sale or merger until after it has occurred – or worse –not until renewal time. The best possible scenario is learning about the sale or merger prior to the actual closing.

When we know beforehand that you are selling your agency, we can advise you and help you understand your E&O policy and the notification requirements.

Whether it is called “change of control,” “mergers and consolidations” or simply “sale, transfer or assignment,” there is a provision in the conditions section of your insurance policy. It seeks to clarify what happens to your insurance policy once you have a majority change in ownership. In some policies, the coverage available under your E&O policy ceases on the date of the sale or merger. Do not be left uninsured because you did not notify us.

WHAT DOES THIS ALL MEAN?

Professional liability policies have an automatic extended reporting period that begins on the date coverage terminates and allows for claims reporting for an additional 30 to 60 days depending on the policy form.

Once your automatic extended reporting period begins, the clock starts ticking off the days that are left for you to purchase the optional extended reporting period or “tail coverage.” If you do not purchase this tail coverage, you could be left uninsured.

Unlike occurrence-based policies, E&O insurance is written on a claims-made basis. This means you must have a policy in force on the day the loss is reported to trigger coverage.

The automatic extended reporting period is typically 30 to 60 days (depending on the policy form) in which you can still file claims for wrongful acts that occurred prior to the cancellation of your policy and after your retro date. Therefore, this extends only the reporting time and not the policy period.

WHAT HAPPENS IF YOUR COVERAGE ENDS?

Here is how it works if your E&O policy has a provision that coverage ceases on the day you have a majority change in ownership:

If you sell your agency effective June 1, the policy coverage terminates. You now have 60 days (approximately August 1) to report any wrongful acts that occurred prior to June 1 but after the retro date on your policy.

If you wish to extend the reporting time (and typically you are required in contract with the buyer to purchase tail coverage) you only have until August 1 to purchase the optional extended reporting period. This ranges from 1 to 10 years depending on the carrier.

Once the 60 days are exhausted, you no longer have the option to purchase tail coverage and you will not have any coverage for wrongful acts that are alleged to have occurred prior to the termination date.

Without coverage, you are now personally responsible for defense and any settlement or judgments that occur. In addition, you are in breach of contract with the buyer.

OIA E&O POLICYHOLDERS

OIA is the agent’s agent. All too often we, your agent, aren’t notified of an agency’s sale or merger until after it has occurred – or worse –not until renewal time. The best possible scenario is learning about the sale or merger prior to the actual closing.

When we know beforehand that you’re selling your agency, we can advise you and help you understand your E&O policy and the notification requirements.

Whether it’s called “change of control,” “mergers and consolidations” or simply “sale, transfer or assignment,” there is a provision in the conditions section of your insurance policy. It seeks to clarify what happens to your insurance policy once you have a majority change in ownership. In some policies, the coverage available under your E&O policy ceases on the date of the sale or merger. Don’t be left uninsured because you didn’t notify us.

WHAT DOES THIS ALL MEAN?

Professional liability policies have an automatic extended reporting period that begins on the date coverage terminates and allows for claims reporting for an additional 30 to 60 days depending on the policy form.

Once your automatic extended reporting period begins, the clock starts ticking off the days that are left for you to purchase the optional extended reporting period or “tail coverage.” If you don’t purchase this tail coverage, you could be left uninsured.

Unlike occurrence-based policies, E&O insurance is written on a claims-made basis. This means you must have a policy in force on the day the loss is reported to trigger coverage.

The automatic extended reporting period is typically 30 to 60 days (depending on the policy form) in which you can still file claims for wrongful acts that occurred prior to the cancellation of your policy and after your retro date. Therefore, this extends only the reporting time and not the policy period.

WHAT HAPPENS IF YOUR COVERAGE ENDS?

Here’s how it works if your E&O policy has a provision that coverage ceases on the day you have a majority change in ownership:

If you sell your agency effective June 1, the policy coverage terminates. You now have 60 days (approximately August 1) to report any wrongful acts that occurred prior to June 1 but after the retro date on your policy.

If you wish to extend the reporting time (and typically you are required in contract with the buyer to purchase tail coverage) you only have until August 1 to purchase the optional extended reporting period. This ranges from 1 to 10 years depending on the carrier.

Once the 60 days are exhausted, you no longer have the option to purchase tail coverage and you will not have any coverage for wrongful acts that are alleged to have occurred prior to the termination date.

Without coverage, you are now personally responsible for defense and any settlement or judgments that occur. In addition, you are in breach of contract with the buyer.

TAKE ACTION NOW

If you are planning an ownership change of your agency, please call your E&O representative to discuss your policy. Already sold or merged your agency? Contact OIA’s E&O team immediately if you are unsure of the next steps — we’ll help you navigate through the E&O process!