The January 2025 reinsurance renewals marked a positive shift for many insurers, as improved market conditions helped stabilize pricing and increase flexibility. At the same time, the excess and surplus (E&S) insurance market continued its growth trajectory—both developments signaling that the broader commercial insurance landscape is adjusting to years of disruption, volatility, and rising demand for risk solutions outside traditional channels.

Reinsurance Renewal Highlights: Capacity and Discipline Return

In contrast to previous years’ tightening conditions, the 2025 reinsurance renewals were notably more favorable for buyers. Stronger capacity, growing reinsurer appetite, and a competitive environment drove more favorable pricing, especially for well-managed portfolios. Brokers noted that clients who entered renewals well-prepared—with robust data and strong loss histories—secured better terms and conditions. (Source: Insurance Journal)

Property catastrophe renewals, in particular, benefited from this dynamic. Large global insurers achieved notable rate reductions, while regional carriers gained much-needed stability. Loss-free programs generally saw single-digit rate decreases, and even loss-hit accounts fared better than they had in 2024.

Despite significant losses from Hurricanes Milton and Helene, reinsurers maintained confidence, backed by improved modeling, capital reserves, and stronger risk segmentation strategies. However, they held firm on higher attachment points, reinforcing the need for insurers to retain more risk—especially in property and casualty lines. This measured approach helped reinsurers better manage mid-sized and attritional losses.

Casualty Reinsurance: Holding the Line Amid Legal Headwinds

Casualty reinsurance renewals remained stable despite pressure from rising litigation costs and adverse loss development trends. Capacity was sufficient to support modest improvements for better-performing portfolios, particularly in excess casualty. That said, reinsurers applied more scrutiny to U.S.-exposed liability renewals, especially in segments where legal, social, or regulatory risks are intensifying.

Market experts like Howden emphasized the importance of portfolio differentiation. Insurers that demonstrated strong claims management, underwriting discipline, and a strategic use of data saw more favorable outcomes. This mirrors broader trends across the industry: well-managed risk is being rewarded, while higher-risk accounts face tougher terms.

E&S Market Growth: A Product of Disruption—and Opportunity

The evolving reinsurance environment is directly influencing the E&S market’s continued expansion. As admitted carriers face stricter reinsurance terms, particularly around catastrophe and liability exposures, more risks are being funneled into the E&S space—where underwriters can respond with greater speed and flexibility.

According to Amwins’ State of the Market—2025 Outlook, the E&S segment now accounts for approximately 34% of the U.S. commercial insurance market, with over $115 billion in written premium in 2023. This growth is underpinned by the same drivers reshaping reinsurance: more frequent extreme weather events, litigation volatility, and a hard market that demands disciplined underwriting (Source: Amwins).

Kevin Doyle, CEO of RPS, noted a philosophical shift among carriers: “There has been a shift in how carriers want to price risks and align their capital with risk.” That shift is pushing more complex, volatile, or unconventional risks into the E&S sector.

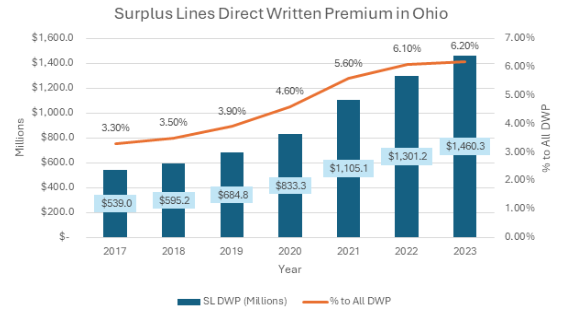

The attached chart showcases the uptick in Surplus Lines direct written premium in Ohio based on our team’s market research.

Innovation and Agility Set E&S Apart

Legal and regulatory headwinds are making it harder for standard markets to respond quickly to emerging threats. E&S insurers, unencumbered by many of the same constraints, are stepping in with tailored solutions, especially in property, casualty, and specialty lines. As Navigators’ Lynanne St. Denis pointed out, E&S insurers are “better positioned to innovate quickly” when faced with emerging risks such as cyber, environmental, or social liability concerns (Source: IA Magazine).

Casualty insurance, in particular, is becoming a greater driver of E&S growth. Jencap reports that “other liability (occurrence)” coverage in the E&S market has nearly doubled since 2020, reflecting rising demand for flexible solutions in sectors affected by legal complexity and social inflation (Source: Jencap).

What’s Next: A Resilient, Evolving Market

Looking ahead, both reinsurance and E&S markets are expected to maintain disciplined underwriting while accommodating more nuanced, data-driven approaches to risk. For the E&S segment, growth is likely to continue well into 2025 and beyond—even with more entrants increasing competition—because of its unmatched ability to underwrite challenging, non-standard risks.

Financial strength and portfolio quality will be key differentiators. Since E&S policies are not backed by state guaranty funds, long-term sustainability depends on maintaining conservative reserves, rigorous underwriting, and thoughtful risk selection.

As traditional and non-traditional markets converge in response to a shifting risk environment, agents and agencies that understand how reinsurance dynamics influence the insurance market will be best positioned to guide clients effectively.

Ohio Insurance Agents: Market Access Support

If you need assistance navigating the E&S or reinsurance marketplace, the Ohio Insurance Agents (OIA) team is here to help. Reach out to Cristie Tillery, Market Access Manager, at cristie@ohioinsuranceagents.com or 614-552-3041.

Coming Soon: The 2024–Q4 Ohio Quarterly P&C Marketplace Summary – available exclusively for OIA members.

About the Author

Jeannine Giesler, CISR, CPIA, and past President of the OIA Board of Directors, Foundation for the Advancement of Insurance Professionals, currently serves as Resource Center Advisor for the OIA. The purpose of the Resource Center is to contribute to building a comprehensive library of resource materials for our members. We pride ourselves on being the one-stop shop for all OIA members and work to solve every problem or situation you may come across.

Jeannine Giesler, CISR, CPIA, and past President of the OIA Board of Directors, Foundation for the Advancement of Insurance Professionals, currently serves as Resource Center Advisor for the OIA. The purpose of the Resource Center is to contribute to building a comprehensive library of resource materials for our members. We pride ourselves on being the one-stop shop for all OIA members and work to solve every problem or situation you may come across.

Legal Disclaimer: This material is intended to provide you with a general background and insight. The material does not constitute and should not be regarded as legal advice regarding any particular facts, circumstances, or issues. This material is not intended to serve as a substitute for legal counsel, and we advise you to contact legal counsel for specific analysis, drafting, and advice.

More Information: Seek your trusted advisors, Attorney, Banker, and CPA to ensure that your legal and financial interests are adequately protected. The information provided in this publication is not intended to be a substitute for legal advice. You should consult your legal counsel and make certain that you are in compliance with state law.

Cited Resources

Reinsurance Buyers with Good Portfolio Stories See Better Renewal Outcomes: Brokers

Insurance Journal By L.S. Howard | January 7, 2025

https://www.insurancejournal.com › news › 2025/01/07

Amwins’ State of the Market—2025 Outlook.

https://www.amwins.com/resources-insights/article/state-of-the-market-2025-outlook

IA Magazine

Why the E&S Market Continues to Grow

19 May 2025 by Olivia Overman

https://www.iamagazine.com/markets/why-the-e-s-market-continues-to-grow

Is the E&S Insurance Market Leveling Out? Trends, Growth, and What’s Next in 2025

Jencap Apr 3, 2025