After several years of rising costs, tightening underwriting, and uneven results, Ohio’s commercial auto market is finally showing signs of stabilization. But while the numbers are improving, the story is far from simple.

Premium growth remains strong. In 2025, Ohio commercial auto direct written premium reached $2.121 billion, up from $1.929 billion in 2024 and just $1.531 billion in 2021. Growth is not the issue.

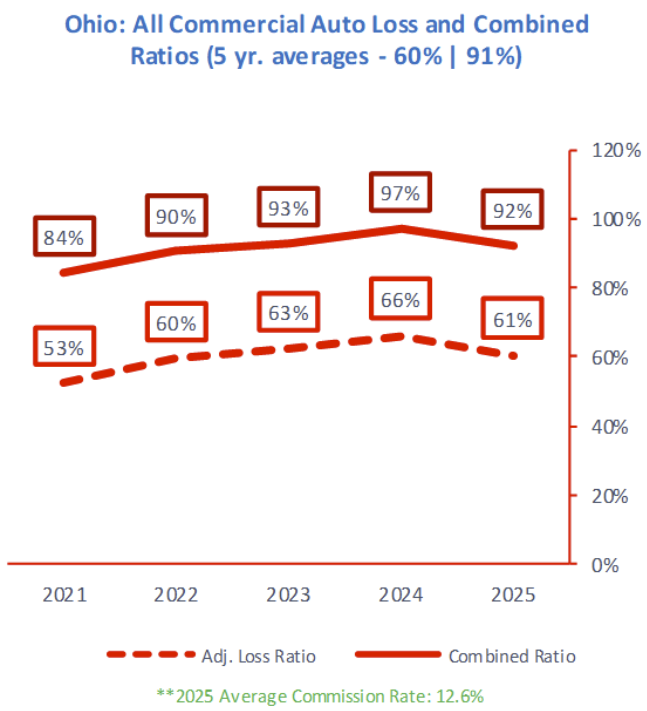

The good news: underwriting results are beginning to rebound. The statewide combined ratio improved to 92% in 2025, down from a recent high of 97% in 2024. Loss ratios followed suit, improving from 66% to 61%.

Still, the market remains sensitive. Loss severity, repair costs, and litigation pressures continue to shape outcomes, and one favorable year does not erase several years of strain. Meanwhile, independent agents continue to dominate distribution, accounting for roughly 90% of the market. In a line of business this complex, their role as trusted advisors has never been more important.

Five-Year Trends in the LOB Market

The past five years tell a clear story: a line under pressure, now beginning to recalibrate.

Premiums climbed steadily from $1.531 billion in 2021 to $2.121 billion in 2025, driven largely by rate increases and exposure growth across key industries like transportation and construction. But underneath that growth, performance told a different story.

- Combined ratios rose from 84% in 2021 to 97% in 2024

- Loss ratios climbed from 53% to 66% over the same period

For several years, carriers were playing catch-up—adjusting rates to keep pace with escalating loss costs. Now, that correction is starting to take hold. In 2025, both combined and loss ratios improved, signaling that pricing and underwriting discipline may finally be aligning with the underlying risk. At the same time, competition remains deep, with 445 active insurers writing commercial auto in Ohio. Even so, the market is far from uniform.

Some carriers are tightening. Others are expanding. Some are prioritizing profitability. Others are chasing growth. That divergence is shaping the next phase of the market.

Carrier Market Leaders in Ohio

The Ohio commercial auto market is no longer moving in a single direction. It’s splitting into distinct strategies—and the top carriers reflect that shift.

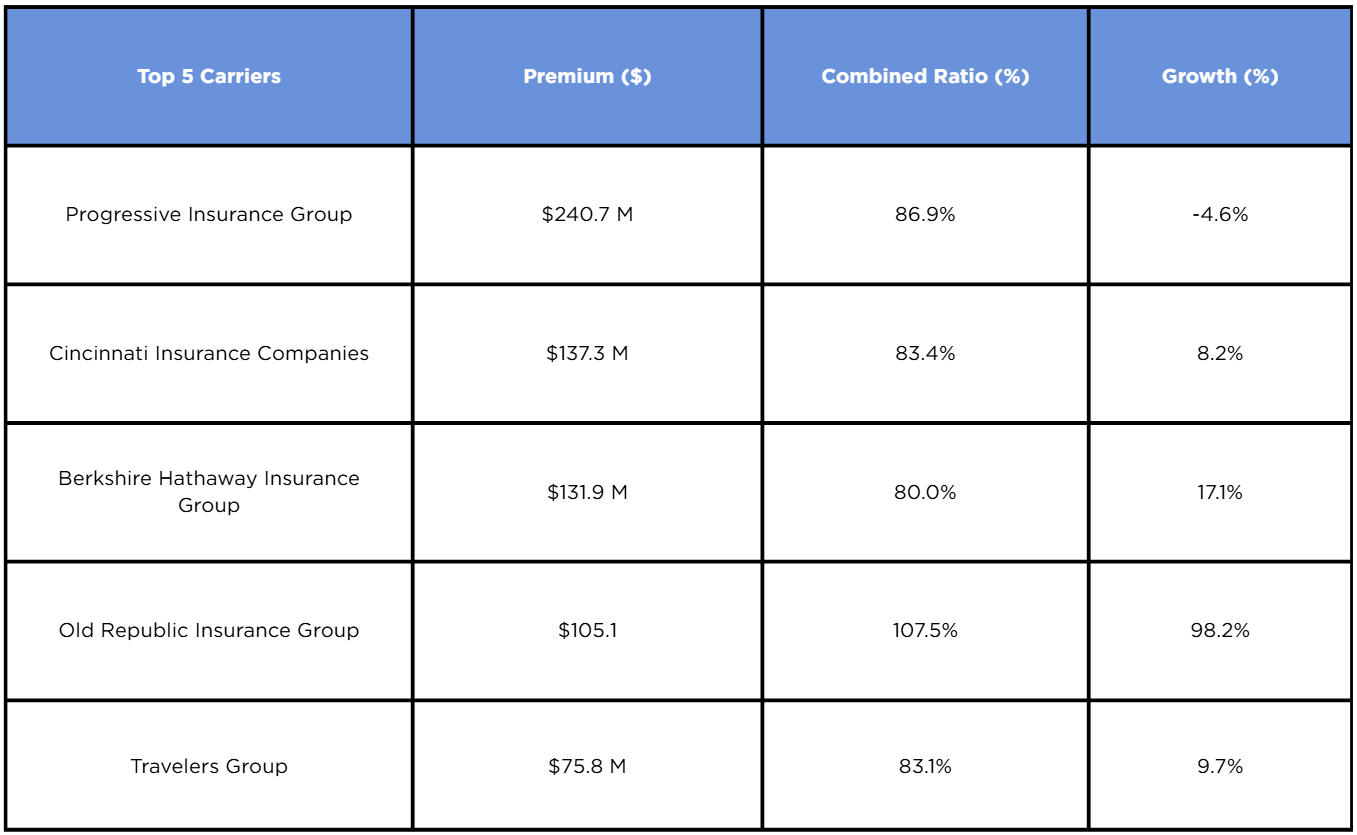

Progressive Insurance Group continues to anchor the market, writing $240.7 million in premium. While slightly down year over year (-4.6%), Progressive maintained strong underwriting discipline with a combined ratio of 86.9%, outperforming the statewide average.

The Cincinnati Insurance Companies stand out as one of the most balanced performers. With $137.3 million in premium and a combined ratio of 83.4%, Cincinnati pairs growth (+8.2%) with profitability—an increasingly rare combination in this line.

Old Republic Insurance Group may be the most disciplined of the group. Its 80.0% combined ratio is the lowest among the top five, demonstrating a clear focus on underwriting performance while still achieving +17.1% growth.

On the other end of the spectrum, Berkshire Hathaway Insurance Group represents a different strategy. Premium surged +98.2% to $132.0 million, signaling aggressive expansion. GEICO Marine Insurance Company was the leading insurer under this group, growing commercial auto premium from $28.2 million in 2024 to $78.8million in 2025 in the Ohio market. However, a combined ratio of 107.5% indicates that growth is coming at the expense of short-term profitability. Greg Abel, CEO, Berkshire Hathaway, shared in a letter to shareholders “The GEICO team remains focused on pricing risks correctly for both existing and new customers. Restoring retention while maintaining underwriting discipline will take time,” according to carriermanagement.com.

Rounding out the top five, Travelers Group delivered steady, measured results with $75.8 million in premium, +9.7% growth, and a solid 83.1% combined ratio.

This is a market of clear tradeoffs:

- Growth vs. discipline

- Expansion vs. profitability

- Market share vs. margin

And carriers seem to be choosing their path with hopes of stabilization over time.

Projections for 2026 and Beyond

Looking ahead, Ohio’s commercial auto market is entering a more balanced, but still cautious, phase.

Premium growth will likely continue, though at a more moderate pace. Much of the heavy lifting from recent years came from rate increases. Going forward, growth will depend more on actual exposure and economic activity. But the bigger question remains: Can profitability hold?

Even with improvement in 2025, the underlying cost environment is still challenging. Repair costs remain elevated due to vehicle complexity. Medical inflation continues to drive claim severity. Litigation trends are not easing. These pressures mean carriers are unlikely to relax underwriting discipline anytime soon. In fact, the opposite is more likely. Expect continued selectivity.

Higher-risk classes, especially transportation and delivery fleets, will remain under scrutiny. Capacity may tighten in certain segments, opening the door for carriers with strong specialization—or agents with the right market access.

Technology will also play a bigger role in shaping the next phase of the market. Telematics, driver monitoring, and data-driven underwriting are no longer optional—they are becoming competitive differentiators. Over time, these tools could help bend the loss curve in a more favorable direction.

Economic conditions will further influence performance. As long as sectors like construction and logistics remain active, demand for commercial auto will follow. Any slowdown, however, could quickly impact exposure growth.

One constant remains: the independent agent. With roughly 90% of the market, agents are at the center of these conversations, helping business owners make sense of pricing, risk, and coverage in an increasingly complex environment.

The outlook? Cautiously optimistic. The market is improving, but it’s not comfortable yet.

Conclusion: What This Means for Agents

In today’s commercial auto market, conversations matter more than ever.

Clients are seeing rate changes, tighter underwriting, and shifting carrier appetites—and they want answers. The most successful agents will be the ones who can clearly connect those changes to broader market trends. Focus on what clients can control:

- Driver safety programs

- Vehicle maintenance

- Use of telematics and monitoring tools

At the same time, position yourself as a strategic partner by exploring multiple carrier options and aligning coverage with each client’s evolving risk profile. The market may be stabilizing, but expertise is still the differentiator.

Sources: carriermanagement.com

About the Author:

Alex Bowie is a marketing professional currently serving as the Senior Manager of Marketing & Communications at the Ohio Insurance Agents Association, Inc. (OIA). In this role, he leads the association’s marketing and communication strategies, elevating OIA’s brand presence and member engagement. His prior experience in the insurance sector—particularly at the insurtech company, Branch—has been instrumental in enhancing OIA’s outreach and engagement efforts.