Other Liability (Occurrence) remained an important but closely watched line in Ohio’s 2025 property and casualty marketplace. The line generally includes liability coverage written on an occurrence basis, meaning coverage is triggered when the injury, damage, or covered event occurs, rather than when the claim is made. For Ohio agents, this line is especially relevant for commercial clients with general liability, umbrella, excess, and other casualty exposures that can be affected by claim severity, litigation trends, contract requirements, and changing underwriting standards.

Other Liability (Occurrence) stood out as one of the state’s more pressured lines, posting an 81.2% Ohio adjusted loss ratio. That result was higher than Ohio’s average loss ratio across all P&C lines and slightly above the U.S. Other Liability (Occurrence) loss ratio of 77.2%, signaling that carriers were continuing to manage casualty risk carefully. For agencies, the line presents both opportunities and challenges.

It is a varied bucket that can include commercial umbrella and excess, standalone general liability for contractors and premises/operations, fiduciary liability, occurrence-based cyber and internet liability, and other casualty exposures. Premium demand remains, but underwriting may be more detailed, especially for accounts with higher limits, complex operations, prior losses, contractual liability concerns, or umbrella and excess needs.

Five-Year Market Trends

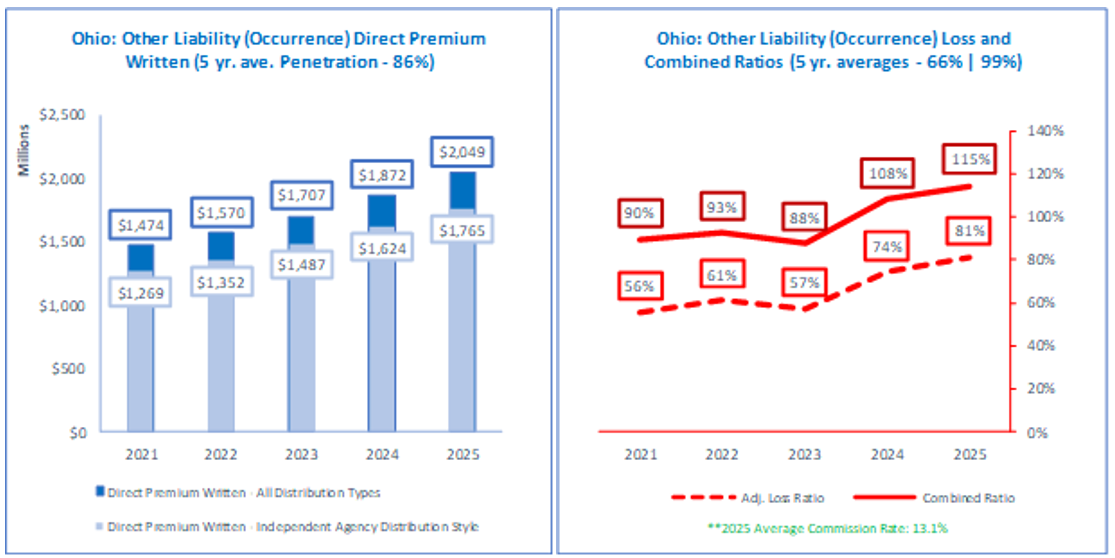

Over the past five years, Ohio’s Other Liability (Occurrence) market has reflected many of the same pressures seen across the broader casualty insurance environment: steady premium growth, more disciplined underwriting, and growing attention to claim severity. From 2021 through 2025, Ohio’s P&C marketplace expanded alongside rising replacement costs, larger liability settlements, and increased demand for higher limits. Other Liability (Occurrence) remained a meaningful part of that growth, especially for commercial accounts with general liability, umbrella, excess, and contractual liability exposures.

The most important trend is that this line has become more sensitive to losses.

By 2025, Ohio’s adjusted loss ratio for Other Liability (Occurrence) reached 81.2%, compared with the state’s overall P&C adjusted loss ratio of 53.9%. That gap shows how casualty lines can create more uncertainty for carriers than many property or personal lines segments. Nationally, Other Liability (Occurrence) also remained under pressure, with a 77.2% adjusted loss ratio and 11.1% premium growth, reinforcing the notion that Ohio’s experience is part of a broader market pattern.

Another key five-year trend is the increased role of surplus lines. Ohio domestic surplus lines premiums represented 5.6% of P&C premiums in 2021 and increased to 6.9% by 2025. That growth suggests more accounts are being placed outside the standard market when risks are complex, higher hazard, or difficult to underwrite. For Ohio agents, the trend points to a market that still offers opportunity but requires earlier renewal planning, stronger submissions, and clearer client conversations about pricing, coverage availability, and liability limit adequacy.

Carrier Market Leaders in Ohio

Carrier leadership in Ohio’s Other Liability (Occurrence) market should be viewed by more than premium size. This line includes a wide range of exposures, including premises liability, completed operations, umbrella, and excess coverage needs. Because of these exposures, agents should look closely at each carrier’s appetite, underwriting focus, capacity, and consistency.

Ohio’s 2025 results show why that matters. Other Liability (Occurrence) posted an 81.2% adjusted loss ratio, which means carriers are likely to stay selective, especially for accounts with complex operations, higher limits, prior losses, contractual liability concerns, or difficult umbrella and excess exposures.

Carrier Market Leaders in Ohio

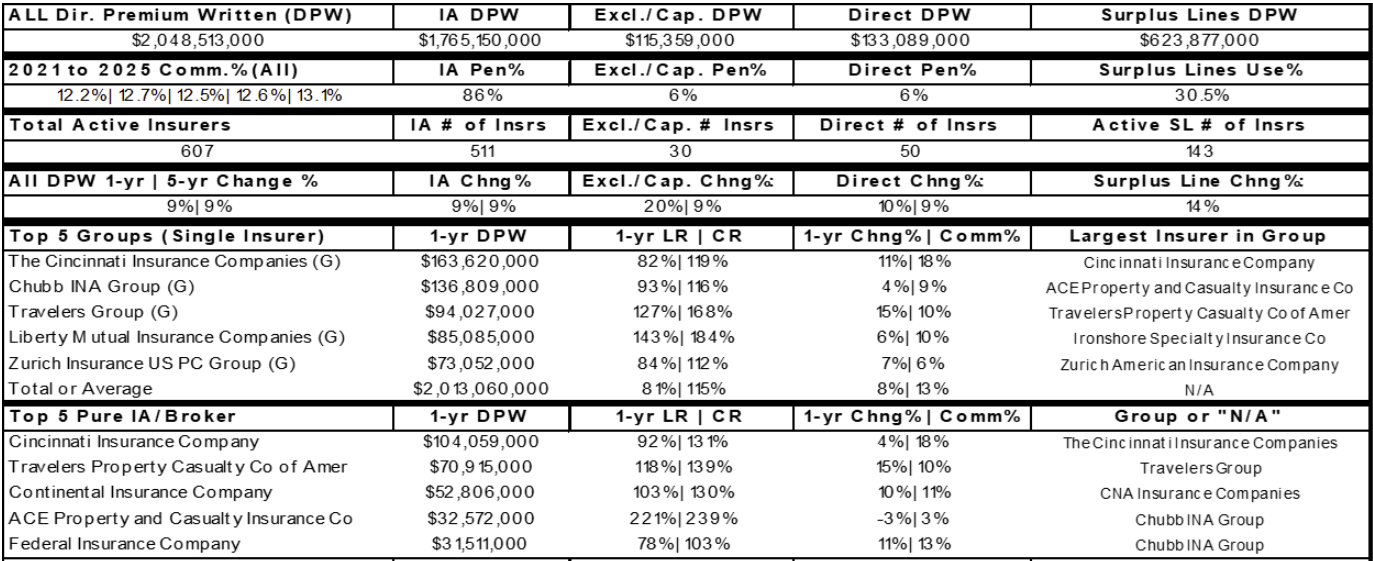

Among the listed top five Ohio carrier groups, Cincinnati Insurance Companies ranked first, writing $163.6 million in Direct Premium Written, with an 82% loss ratio and 119% combined ratio. Chubb INA Group followed with $136.8 million in DPW, a 93% loss ratio, and a 116% combined ratio. Travelers Group ranked third with $94.0 million in DPW, but its 127% loss ratio and 168% combined ratio show the severe pressure affecting this line.

Liberty Mutual Insurance Companies ranked fourth, writing $85.1 million in DPW, with a 143% loss ratio and 184% combined ratio. Zurich Insurance US PC Group rounded out the top five with $73.1 million in DPW, an 84% loss ratio, and a 112% combined ratio.

The key takeaway is that premium leadership does not always equal underwriting profitability. Several top carriers posted combined ratios above 100%, signaling continued concern around pricing, loss development, claim severity, and expenses. For Ohio agents, the most useful carrier partner is not only the one with market share, but the one with the right appetite, responsiveness, claims handling, and willingness to support the client’s specific risk profile. Strong submissions, clear exposure details, and early renewal conversations will be important when working with these market leaders.

Projections for 2026 and Beyond

Ohio’s Other Liability (Occurrence) market is expected to remain disciplined in 2026 and beyond. While overall commercial insurance conditions are becoming more segmented, casualty lines are not softening at the same pace as property or workers’ compensation. National market outlooks point to continued pressure in general liability, umbrella, and excess liability, with rate movement still tied closely to loss history, class of business, venue, limits, and attachment points. For Ohio, the 2025 adjusted loss ratio of 81.2% suggests carriers will continue to watch profitability carefully before expanding appetite or offering broader terms.

Future performance will be shaped by several factors. Claim severity is the most important. Larger settlements, higher defense costs, nuclear verdicts, and third-party litigation funding continue to push liability loss costs upward. Even when claim frequency is stable, a small number of severe claims can materially affect results for occurrence-based liability coverage. Commercial auto liability will also influence umbrella and excess performance because auto-related losses often pierce underlying limits and affect higher layers.

Capacity should remain available for well-managed accounts, but it may be more selective for higher-hazard operations, poor-loss accounts, habitational risks, construction, products liability, and accounts needing large umbrella towers. Specialty and surplus lines markets are likely to remain important, especially when admitted carriers reduce limits, tighten terms, increase attachment points, or require stronger underlying coverage. As more carriers use data analytics, risk controls, and class-specific underwriting, clients with documented safety practices, clean loss runs, and complete exposure information may see better outcomes.

Pricing in 2026 will likely vary by segment. Preferred and lower-hazard accounts may experience moderate increases or more competition, while challenging risks may continue to see firm pricing, reduced capacity, or layered placements. Combined ratios above 100% among several Ohio top five carriers also suggest that underwriting discipline will remain a priority.

For Ohio agents, the outlook calls for proactive renewal management. Agents should start conversations early, review contracts and additional insured obligations, confirm operations and payroll or sales changes, and help clients understand why liability limits and attachment points matter. The agencies that provide complete submissions and explain market pressures clearly will be best positioned to preserve options in a market that remains opportunity-rich but loss-sensitive.

Conclusion: Client Conversation Tips

When talking with clients about Ohio’s Other Liability (Occurrence) market, keep the conversation practical. Explain that carriers are reviewing this line more carefully because loss severity, litigation costs, and umbrella or excess exposures can drive claims higher. Encourage clients to review current limits, contracts, additional insured requirements, completed operations exposures, and changes in payroll, sales, or operations. Start renewals early and gather updated loss runs, safety information, and risk-control details. Position the conversation around preparedness: better information helps preserve market options, supports stronger underwriting discussions, and reduces surprises when pricing, terms, or capacity change.

Sources:

2026 Ohio Annual P&C Marketplace Summary, Real Insurance Solutions Consulting, LLC, Paul A. Buse, Principal, 2026. Used for Ohio-specific P&C marketplace context, Other Liability (Occurrence) loss ratio, premium growth, independent agent penetration, and surplus lines trends.

Other Liability (Occurrence)-Impact of litigation trends on projections

Rising Nuclear Verdicts and Litigation Funding a New Reality for US Casualty Insurers

2025 Q4 Umbrella and Excess Market Update

2026 Q2 Umbrella and Excess Market Update

About the Author

Jeannine Giesler, CISR, CPIA, and past President of the OIA Board of Directors, Foundation for the Advancement of Insurance Professionals, currently serves as Resource Center Advisor for the OIA. The purpose of the Resource Center is to contribute to building a comprehensive library of resource materials for our members. We pride ourselves on being the one-stop shop for all OIA members and work to solve every problem or situation you may come across.

Jeannine Giesler, CISR, CPIA, and past President of the OIA Board of Directors, Foundation for the Advancement of Insurance Professionals, currently serves as Resource Center Advisor for the OIA. The purpose of the Resource Center is to contribute to building a comprehensive library of resource materials for our members. We pride ourselves on being the one-stop shop for all OIA members and work to solve every problem or situation you may come across.