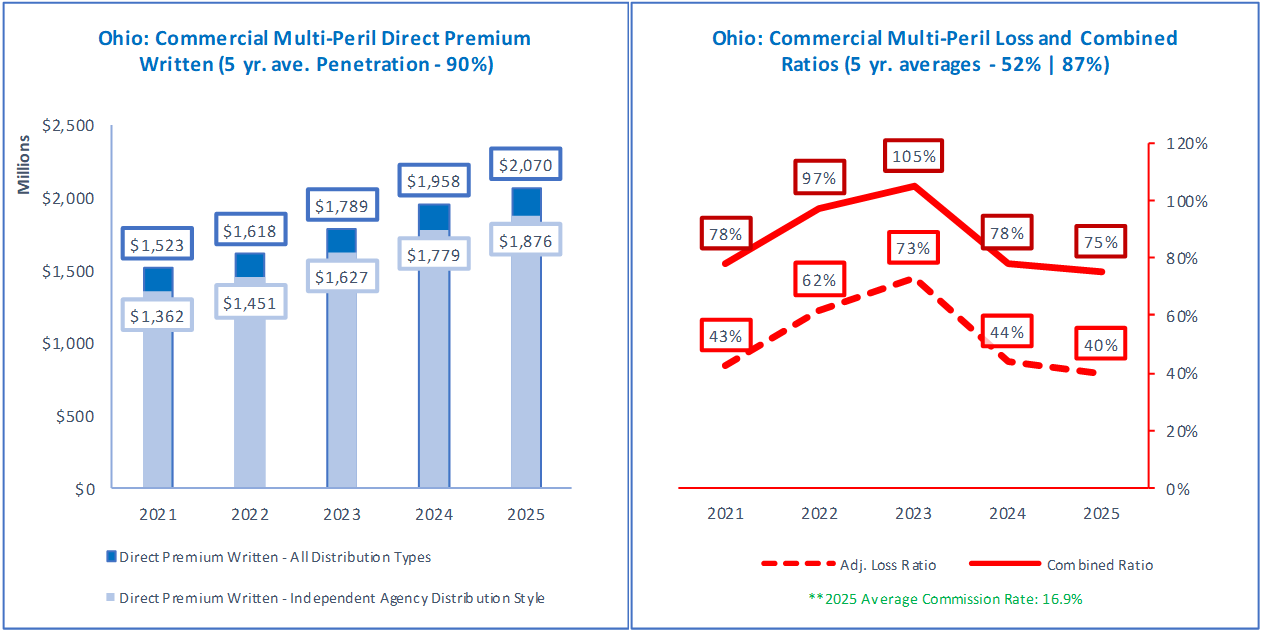

Over the past five years, Ohio’s commercial multi-peril market has shown steady, meaningful growth, with direct written premium rising from roughly the mid-$1 billion range to more than $2 billion. That upward climb signals continued demand for packaged commercial coverage among Ohio businesses, even as the broader property and casualty market has faced inflation, evolving risk exposures, and shifting underwriting conditions. With a five-year average penetration rate of 90%, commercial multi-peril remains a major line of business in the state and a key coverage area for independent agencies serving small and mid-sized commercial clients.

Commercial multi-peril insurance remains a cornerstone of Ohio’s business insurance marketplace, and the 2025 data reveals a compelling mix of regional strength and national competition. Cincinnati Insurance Companies sits firmly at the top with more than $272 million in direct written premium, supported by a strong 13.9% share of the national CMP market and a healthy 66.7% combined ratio. The company’s premium growth of 6.2% from 2024 to 2025 demonstrates continued momentum in a line where disciplined underwriting and long-term agency relationships remain critical to success.

What’s particularly noteworthy is the performance of Ohio-based carriers. Westfield Group, Cincinnati Insurance, and Erie Insurance Group all rank among the state’s top commercial multi-peril writers, highlighting Ohio’s outsized influence in this important commercial line. Erie posted the strongest premium growth among the top five carriers at 9.7%, while Westfield’s 21.0% share of the U.S. commercial multi-peril market underscores the company’s national reach despite its Ohio roots. Together, these insurers showcase the strength of the independent agency channel, providing businesses across Ohio with access to carriers that combine local market knowledge with proven underwriting expertise.

The data also points to a profitable and relatively stable marketplace. Every carrier in the top five reported a 2025 combined ratio below 82%, with Cincinnati, Travelers, and Auto-Owners all posting ratios in the mid-to-upper 60s. In a period marked by economic uncertainty, inflationary pressures, and evolving risk exposures, those results suggest that commercial multi-peril continues to be a well-managed and attractive line of business. For Ohio independent agents, that’s encouraging news: strong carrier performance often translates into continued market capacity, investment in agency partnerships, and competitive options for commercial clients.

In short, Ohio’s commercial multi-peril market isn’t just growing—it’s thriving. The presence of several high-performing, agency-focused carriers at the top of the rankings reinforces the state’s reputation as a stronghold for the independent agency system and a leader in commercial insurance innovation and profitability.

Broader Commercial Market Trends

While commercial multi-peril remains one of Ohio’s strongest commercial lines, it does not operate in isolation. Broader commercial market trends continue to influence carrier appetite, pricing, underwriting performance, and risk placement strategies across the industry.

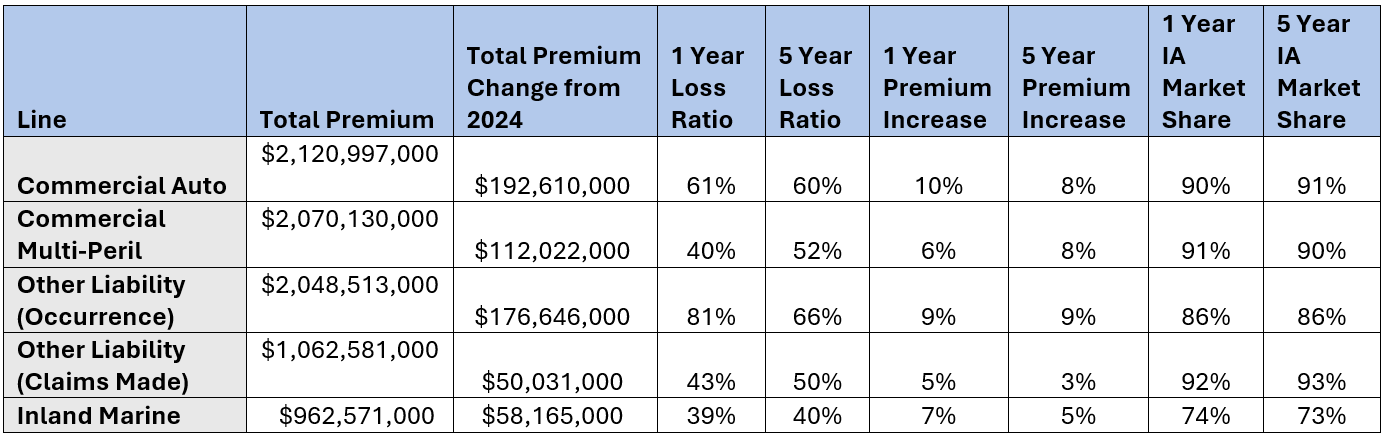

Below is a summary of the top five commercial lines by total premium, loss trends, and IA market share in Ohio.

Consistent with loss ratio trends, Ohio saw the largest premium increases in 2025 in Commercial Auto (10%), Other Liability (Occurrence) (9%), and Farmowners Multi-Peril (9%).

Together, these trends point to a market that remains financially healthy overall but continues to evolve. While underwriting results have improved in many areas, agents are navigating a landscape marked by increasing specialty-market utilization, uneven performance across lines of business, and growing complexity in commercial risk placement.

Loss Ratio Pressures

Despite improving results in several commercial lines, Ohio insurers continue to face many of the same challenges affecting the broader marketplace. Economic inflation, severe weather events, increasing claim frequency, and rising commercial auto losses continue to put pressure on underwriting performance. At the same time, social inflation remains a significant concern, as larger jury awards, higher settlement costs, and increasing litigation expenses drive claim severity higher across liability lines.

Commercial Auto continues to be one of the most difficult lines in the market, with liability losses and loss adjustment expenses worsening each year since 2016. Meanwhile, increasing weather frequency and severity continue to contribute to higher losses in crop insurance, reinforcing the volatility present in agricultural risks.

There may be reason for optimism on the liability front. Earlier this year, OIA’s advocacy team helped advance legislation aimed at increasing transparency around third-party litigation funding, a practice often cited as a contributor to rising claims costs and social inflation. The bill has passed both chambers of the Ohio General Assembly and is awaiting the Governor’s signature.

How Can Agents Respond to Commercial Market Trends?

Independent agencies remain well positioned to compete and grow in Ohio’s commercial insurance market, where they continue to write nearly 90% of commercial policies. Yet today’s marketplace is becoming more complex. While overall market conditions have improved in some areas, agencies are navigating a combination of social inflation, rising litigation costs, severe weather activity, technology-related risks, fraud exposure, and ongoing economic inflation. In May 2026, inflation reached 4.2%, continuing to drive up the cost of repairs, replacement materials, and labor. At the same time, the United States experienced 23 separate billion-dollar weather disasters in 2025, underscoring the growing impact of catastrophe losses on the insurance industry.

These trends are contributing to a continued shift toward excess and surplus (E&S) markets as more risks fall outside the appetite of standard carriers. Small and mid-sized businesses increasingly face exposures that require specialized underwriting solutions, creating both challenges and opportunities for independent agents. Agencies that can effectively educate clients, access specialty markets, and provide proactive risk guidance will be best positioned to strengthen relationships and retain business.

According to the 2026 State of the Market Outlook from AMWins, agencies should approach renewals strategically and treat each account as a unique opportunity. Strong renewal preparation begins with a thorough evaluation of the account’s specific risk characteristics, operational changes, and loss history. Up-to-date valuations are also critical, helping clients avoid coinsurance issues, valuation gaps, and future premium shocks when market conditions tighten. Detailed loss summaries, including explanations of significant claims and corrective actions taken, can improve underwriting outcomes and help carriers better understand an account’s risk profile.

Submission quality continues to matter. As underwriters manage record submission volumes, well-organized and comprehensive applications are more likely to receive favorable attention. For larger or more complex accounts, agencies should consider meeting proactively with incumbent and prospective carriers to discuss risks, expectations, and renewal strategies. Thoroughly reviewing quoted terms, conditions, exclusions, deductibles, and risk-management requirements has also become increasingly important as carriers continue to refine underwriting standards.

Beyond placement strategy, agencies should continue investing in specialization and operational efficiency. Developing expertise within specific industries allows agencies to move beyond transactional insurance sales and become trusted advisors. As risks become more sophisticated, businesses increasingly value advisors who understand the unique challenges facing their industry and can provide guidance beyond coverage placement alone.

Operational improvements are equally important. Every hour spent on administrative work is time that cannot be devoted to client relationships, prospecting, or strategic planning. Agencies that invest in support staff, operational leadership, automation, or virtual assistance can create more capacity for growth while maintaining a high level of client service. OIA’s partnership with Next Level Partners provides additional resources to help agencies train and develop the next generation of commercial insurance professionals.

Conclusion

Ohio’s commercial multi-peril market continues to demonstrate the strength of both the state’s business community and its independent agency system. Strong premium growth, favorable underwriting results, and a highly competitive carrier landscape have helped make CMP one of Ohio’s most successful commercial lines.

At the same time, broader commercial market trends underscore the challenges that lie ahead. Rising liability costs, catastrophe exposure, economic pressures, and growing reliance on specialty markets will continue to shape the marketplace. Success in the years ahead will belong to agencies that combine strong client relationships with industry expertise, operational excellence, and a proactive approach to risk management. As the market continues to evolve, independent agents remain uniquely positioned to help Ohio businesses navigate complexity, secure appropriate coverage, and thrive in an increasingly challenging risk environment.

Sources:

AMWins 2026 State of the Market Outlook Report

About the Author

Brian Lawrence is the Sr. Director of Agency Talent Development for Ohio Insurance Agents. He is responsible for providing HR support and resources for the membership. His HR career spans 25 years across Insurance, Financial Services, Healthcare, and Association Management.

Brian Lawrence is the Sr. Director of Agency Talent Development for Ohio Insurance Agents. He is responsible for providing HR support and resources for the membership. His HR career spans 25 years across Insurance, Financial Services, Healthcare, and Association Management.

Much of his experience includes 20 years at Nationwide, where he spent seven years as an HR Director/HR Business Partner providing strategic support to executive leadership teams across P&C, Commercial and Non-Standard Customer Service Operations, Life Insurance and Annuity Operations, & Nationwide Pet Insurance.