The insurance market today is offering a rare and uneasy mix of signals. Pricing is beginning to ease and capacity is becoming more available, yet underlying risk factors remain elevated. Many describe this environment as a “soft market under stress”—a temporary window of opportunity that could close quickly.

For agents, the challenge is not predicting exactly when the cycle will turn. The real opportunity lies in helping clients act wisely while conditions are favorable, without assuming those conditions will last.

What the Data Is Showing

As an OIA member, you now have access to the 2025 Q3 Ohio Quarterly P&C Marketplace Summary, delivered as part of your membership benefits. The report provides an up‑to‑date view of Ohio’s property and casualty market using direct premiums before reinsurance, supported by the most recent A.M. Best data available as of July 13, 2025.

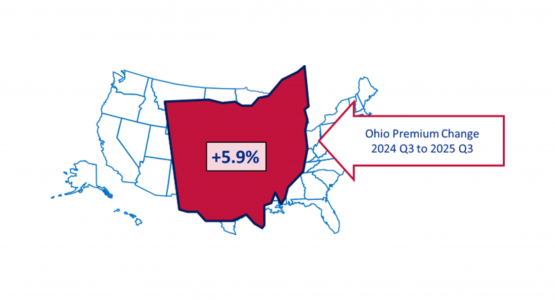

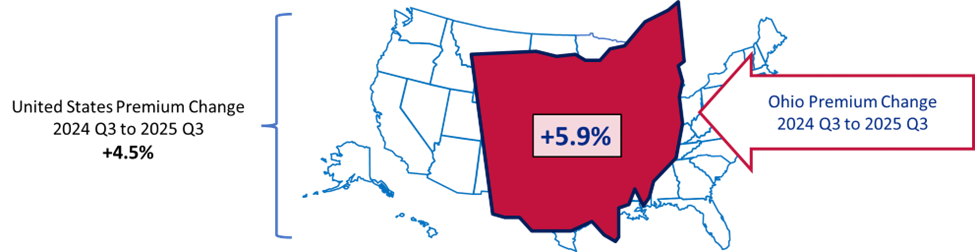

At a national level, premium growth continues to slow. After exceeding 10 percent in 2023, total P&C premium growth moderated to 4.5 percent by Q3 2025. Ohio remains slightly ahead of that pace, with premium growth of 5.9 percent over the same period. Homeowners and Other Liability (Occurrence) continue to be among the fastest‑growing lines nationwide.

Loss experience has been relatively calm overall, though performance varies by geography. The loss picture contrasts sharply with 2024, when significant convection and flood activity—particularly in the second quarter—drove notable spikes in losses across both Ohio and the broader U.S. market.

Line‑Specific Performance Tells a Mixed Story

Private Passenger Auto remains a bright spot in Ohio. Direct underwriting gains were recorded in four of the five most recent completed years, with a five‑year average combined ratio of approximately 90 percent in Ohio versus 95 percent nationwide. From an agent’s perspective, those results represent a favorable return on premium dollars before investment income, even after accounting for reinsurance participation.

Commercial Auto tells a different story. While Ohio has performed materially better than the national average, pressure remains evident. The U.S. market continues to post five‑year average combined ratios above 100, and Ohio’s results moved closer to breakeven in 2024 at 97 percent, underscoring the ongoing challenges in this line.

Among the top 10 direct premium insurers nationally and in Ohio, 2025 data shows relatively slow premium growth and stable losses. This stability is notable when compared with the volatility seen in 2024 and reinforces the idea that current market conditions are favorable—but not guaranteed.

The Independent Agency Channel Remains Well‑Positioned

The Big “I” 2025 Market Share Report, based on 2024 data, confirms that the independent agency channel continues to hold its ground. Market penetration remains steady, combined loss ratios have improved, and direct written premiums continue to grow. These fundamentals reinforce the strength of independent agents during periods of transition and market uncertainty.

Why Today’s Market Requires a Balanced Message

While conditions may feel “soft” in certain lines—particularly Property, Cyber, and D&O—loss costs are still climbing in casualty‑driven segments such as Auto and general liability. That divergence creates both opportunity and risk.

In the short term, pricing is competitive and capacity is widely available. The percentage of customers who shopped for auto insurance hit record-high levels at 57% in 2025, up from 49% in 2024, according to JD Power. However, unlike past years – when switching lagged shopping – customers are finding better prices in the market, which will put further pressure on insurers throughout 2026. In the medium term, a major catastrophe, geopolitical shock, or capital disruption could reverse course quickly. Over the long term, volatility is likely to remain a defining feature of the market.

Agents don’t need to predict the next turn of the cycle to add value. What clients need most is context.

How Agents Can Help Clients Act Now

This environment offers a rare degree of carrier flexibility. Coverage terms can often be broadened, limits increased, and program structures improved without significant cost impact. Long‑standing coverage gaps that were difficult to address in recent years can finally be closed.

It is also an ideal moment to secure stability. Multiyear policies, rate guarantees, and longer capacity commitments are easier to negotiate when the market is receptive. Locking in today’s pricing can provide meaningful protection against future volatility.

Equally important is shifting conversations away from price alone. Helping clients focus on their total cost of risk—including safety practices, documentation, cyber controls, and analytics—positions them more favorably when underwriting conditions tighten again.

Strategic Considerations by Line of Coverage

Property markets show signs of accelerating softness. Now is the time to reassess valuations, secure appropriate limits ahead of catastrophe seasons, and consider adding higher‑risk CAT coverage while pricing remains competitive.

Cyber remains historically soft, but that softness depends heavily on continued loss performance. Encouraging clients to use current savings to increase limits—while ensuring cyber hygiene requirements are up to date—can pay dividends later.

D&O pricing remains favorable, though momentum appears to be slowing, particularly for large public companies and financial institutions. Agents should use current conditions to renegotiate terms before additional carrier capacity exits the space.

Casualty and Auto continue to demand discipline. Loss control, safety initiatives, and data‑driven insights remain essential, and some clients may need to prepare for higher retentions or alternative risk solutions.

The Message That Resonates with Clients

The most effective message to clients is a simple one:

“Today’s soft market is an opportunity—but it’s temporary. Let’s strengthen your program now, so you’re better protected if conditions change sooner than expected.”

Clients understand risk. What they value most is foresight.

Agents who guide clients through both the present opportunity and the potential challenges ahead don’t just place coverage—they build durable, long‑term relationships.

About the Author

Jeannine Giesler, CISR, CPIA, and past President of the OIA Board of Directors, Foundation for the Advancement of Insurance Professionals, currently serves as Resource Center Advisor for the OIA. The purpose of the Resource Center is to contribute to building a comprehensive library of resource materials for our members. We pride ourselves on being the one-stop shop for all OIA members and work to solve every problem or situation you may come across.

Jeannine Giesler, CISR, CPIA, and past President of the OIA Board of Directors, Foundation for the Advancement of Insurance Professionals, currently serves as Resource Center Advisor for the OIA. The purpose of the Resource Center is to contribute to building a comprehensive library of resource materials for our members. We pride ourselves on being the one-stop shop for all OIA members and work to solve every problem or situation you may come across.

Cited Sources

Big ‘I’ Releases 2025 Market Share Report July 17, 2025

By: AnneMarie McPherson Spears

BIG I 2025 Market Share Report

Good Times for U.S. P/C Insurers May Not Last; Auto Challenges Ahead Claims Journal

By Susanne Sclafane | January 9, 2026

JD Power January 29th 2026

Q4 2024 – Insurance Shopping List Report

23 January 2026

Rate Pressure, Customer Retention and Digital Engagement Top Insurance Industry Challenges for 2026